Bridges Limited founder Chibamba Kanyama says refinancing of Zambia’s Eurobonds will worsen the country’s debt position and make it practically impossible for future generations to govern.

Last month, President Edgar Lungu hinted that an unnamed Turkish company had expressed interest in refinancing Zambia’s US $750 million Eurobond during an unprecedented visit by his Turkish counterpart, Recep Tayyip Erdoğan at State House.

Commenting on the development in an interview with News Diggers! Kanyama said refinancing may not necessarily be relief, and will make Zambia’s debt position eat away the entire government cash flows in the long-run as it will be extremely unsustainable.

He cautioned that future generations would grapple with the country’s growing debt problem, making it difficult to govern the country.

“The IMF is not concerned about Zambia’s efforts to refinance its current Eurobonds or any other loans when they fall due except that refinancing may just worsen the problem and make it practically impossible to even talk to the Washington, D.C.-based lender. The IMF has assessed the current Zambian indebtedness is unsustainable and being at high risk of default. If the Zambian government manages to refinance the Eurobonds even earlier than the time they fall due, it may potentially offer some relief on the current high interest payments. You may know that nearly 30 per cent of our revenues is in interest rates pay-outs and this may rise by next year when the debt/GDP ratio reaches 70 per cent as predicted by many authorities and economists,” Kanyama said in Lusaka, Monday.

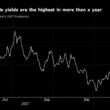

“It is, however, important to know that, refinancing may not necessarily be relief. The Eurobond is currently trading at yield rates of around 11 per cent, which is over 2.5 basis points Zambia secured the Eurobond. This in itself tells you whoever finances the Zambia loan will seek a premium, well over 11 per cent and this is 300 per cent over our current GDP growth rate. There is one reason I am discouraging government from refinancing its loan, and I have firm belief the IMF may hold the same view: refinancing will definitely make Zambia’s debt position eat away the entire government cash flows in the long-run as it will be extremely unsustainable, disabling the country’s own capacity to generate incomes, inadequate social sector spending, increase poverty levels by huge margins, threaten national security as we witnessed in some Latin American countries as Argentina, Venezuela and Brazil, and make it nearly impossible for the generation that will take hold of the country 15 years from now to govern properly.”

He said refinancing only works well under circumstances where government is fully convinced that economic fundamentals in future, such as the exchange rate regime, economic growth and earnings from the key export products, such as copper, would be far much better.

“Refinancing can only come from the external private market because without an IMF programme, no cooperating partner will be willing to offer any relief, let alone increase the budget support thresholds. Refinancing simply means incapacity to settle current debts and this is the time governments usually attract non-conventional lenders, such as vulture funds, who seek to leverage desperate situations. I am very sure government is very awake to this danger. Refinancing only works well under circumstances where government is fully convinced that economic fundamentals in future, such as the exchange rate regime, economic growth, earnings from the key export products, such as copper in our case, will be far better than the current situation holds,” Kanyama explained.

He advised government to instead fully implement the austerity measures and pay back the first Eurobond, which matures in 2022.

“It is only under those circumstances you can refinance an existing loan. My firm advice to government, which would be the same advice IMF may give, is that we must apply the self-engineered austerity measures and settle the Eurobonds in full as they mature starting in 2022. Refinancing is never an option when we are uncertain about what the future holds. We may even be far more vulnerable in future than we [are] now, so, the decision to settle the Eurobonds is squarely in our hands and there are many of us citizens willing to support government on this score. Let us not postpone a problem for the future generation to contend with. We created it and, therefore, we must be magnanimous enough to resolve it,” advised Kanyama.

Aside from Zambia’s external debt stock, which currently sits at US $9.37 billion as at the end of first quarter, the country’s growing domestic debt to K51.86 billion as at end June this year, continues to pose challenges to government’s fiscal management.

According to Finance Minister Margaret Mwanakatwe, government has so far paid US $161.3 million in external debt servicing by June, 2018.

Last month, she announced that government already exceeded its budget for the first half of 2018 by K5 billion owing to huge interest payments and capital expenditure.

Additionally, the Ministry of Finance’s supplementary budget of K7.2 billion, roughly US $721 million, was approved in Parliament last month.

And out of the total, K3.6 billion is for domestic and external debt obligations, while K1.3 billion will be spent on completing infrastructure projects and K2.3 billion will cover shortfalls on government-support programmes, by-elections and the recruitment of a further 3,700 medical personnel.